The Chancellor, Rachel Reeves, presented her Budget statement on 26 November 2025.

This is a brief round up of the main announcements affecting individuals and small business tax:

- Personal tax and National insurance:

- All main income tax and national insurance threshold will remain frozen until the end of the 2030-31 tax year (some allowances, such as the blind person’s allowance, continue to be uprated in line with inflation). This is an extension to the previously announced freeze, which was due to end in April 2028.

- The lower earnings limit will increase to £6,708 (from £6,500) – this is the earnings at which employees receive a credit towards their state pension. This means that director-shareholders still needing state pension credits will need a salary of at least £6,708, which may mean their comany paying some employer national insurance.

- Employer national insurance

- The employer NI threshold (secondary threshold) will remain at £5,000 until the end of the 2030-31 tax year.

- Pension contributions

- From April 2029, the amount that is exempt from National Insurance contributions (NICs) under salary sacrifice for pension contributions will be capped at £2,000 a year.

- Employer contributions will continue to be free of NICs.

- Non-earned income tax rates

- Dividends: The tax rate on dividends will increase by 2 percentage points from 6 April 2026. This means that dividends in the basic rate will be taxed at 10.75% and higher rate will be 35.75%. There is no change to the additional rate, which remains at 39.35%.

- Savings income: Tax on savings income will increase by 2 percentage points across all bands from 6 April 2027. The basic rate will rise from 20% to 22%, the higher rate from 40% to 42%, and the additional rate from 45% to 47%.

- Property income: The government is creating separate tax rates for property income. From April 2027, the property basic rate will be 22%, the property higher rate will be 42% and the property additional rate will be 47%. Finance cost relief will be provided at the separate property basic rate (22%).

- The income tax ordering rules will be changed from April 2027 so that the Personal Allowance will be deducted against employment, trading or pension income first.

- Corporation tax

- There were no changes to the rates of corporation tax.

- The late filing penalty for corporation tax returns will double (to £200 for the initial penalty) from 1 April 2026.

- Capital allowances

- From April 2026, the rate of writing-down allowance (WDA) on the main pool of plant and machinery will reduce from 18% to 14% per year. This will mainly affect businesses with pools of historic expenditure, as well as specific other asset purchases such as cars, since most capital spend can now be fully expensed (for companies), or is covered by the annual investment allowance (for companies and unincorporated businesses).

- From January 2026, there will also be a new 40% first year allowance for spend applying to certain assets where full expensing or the annual investment allowance is not available. (Note: this will not be available for cars or second hand assets).

- (Note: these measures are irrelevant for most small businesses, apart from in relation to receiving a smaller writing down allowance on low emission vehicles, since most of their expenditure is covered by the annual investment allowance).

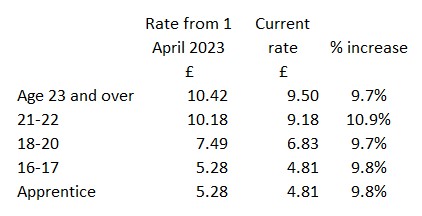

- Minimum Wage

- The national living wage will increase to £12.71 (by 4.1%) with effect from April 2026.

- The national minimum wage for 18-20 year olds will increase to £10.85 (8.5%), continuing the narrrowing of the gap between that and the NLW with a view to eventually creating a single adult rate.

- The apprentice rate (and presumably the under 18 rate) will increase from £7.55 to £8.00 (6%) per hour.

- Capital gains tax

- There were no changes to the rates or allowances for capital gains.

- Inheritance tax

- IHT rates and thresholds remain unchanged and the thresholds will now be frozen until 2031 (a one-year extension to the previous freeze).

- The £1m allowance announced for Agricultural and Business property announced in the 2024 Budget will be trasferreable between spouses and civil partners.

- Property:

- The government is introducing a High Value Council Tax Surcharge (HVCTS) in England for residential properties worth £2 million or more, from April 2028. The charges start at £2,500 per year, rising to £7,500 per year for properties valued above £5 million, and will be levied on property owners rather than occupiers.

- As mentioned above, tax rates on property income will increase by 2 percentage points from April 2027.

- Savings

- ISA threshold total remains unchanged, however the cash ISA limit will be reduced to £12,000 for those under 65 from April 2027. This means that, to invest the full limit, at least £8,000 must be invested in stocks and shares.

- As mentioned above, tax rates on savings will increase by 2 percentage points from April 2027, and the tax rate on dividends in the basic and higher rate band will increase by 2 percentage points from April 2026.

- VAT

- The VAT registration thresholds remain unchanged

- Motoring

- Fuel duties will be frozen until August 2026, after which rates will increase, gradually returning to March 2022 levels by March 2027.

- There will be a new Electric Vehicle Excise Duty (eVED) from April 2028. This will be a 3p per mile charge for full EVs and 1.5p for plug in hybrids (PHEVs).

- Other indirect taxes

- Fuel duties will be frozen until August 2026, after which rates will increase, gradually returning to March 2022 levels by March 2027.

- Alcohol duties will increase in line with RPI with effect from 1 February 2026

- Other announcements

- MTD ITSA penalties: There will be no late filing penalties for quarterly reports under MTD in 2026-7. Penalties will still apply if the final filing is late though.

- Coding of self assessment tax payments: The government will require income tax Self Assessment taxpayers with Pay As You Earn (PAYE) income to pay more of their Self Assessment liabilities in-year via PAYE from April 2029. The government will publish a consultation in early 2026 on delivering this change, and on timelier tax payment for those with only Self Assessment income

- Tax relief for working from home: From April 2026, employees will no longer be able to claim a tax deduction (the £6 per week that many claimed during Covid) for additional costs of working from home where these are not reimbursed by their employer. (This measure will not impact the existing ability for employers that reimburse employees for costs relating to homeworking where eligible without deducting Income Tax and National Insurance contributions.) (Note: I suspect that many have continued to claim post-Covid when they are probably not entitled, so it is simpler to just stop all claims than challenge them one by one!)

- In-year reporting of dividends: The government will publish a consultation in early 2026 to explore introducing new requirements to report transactions between close companies and their shareholders to HMRC. The effect of this would be that owner managed businesses would have to report the dividends paid to their shateholders as they were paid.