Following the disastrous ‘Mini-Budget’ in September, and the subsequent confusion and u-turns, the Chancellor, Jeremy Hunt, presented his Autumn Statement on 17 November 2022.

The statement, unlike the September statement, was fully supported by OBR (Office for Budgetary Responsibility) forecasts.

There has been a lot of speculation regarding tax increases over the past few weeks, may of which came to fruition, but, fortunately, three of the touted changes in respect of an increase in the rate of capital gains tax, an increase in the rate of dividend and a restriction in pension tax relief tax did not feature.

The main announcements relating to personal tax and small businesses were:

- Most income tax, national insurance and inheritance thresholds will be frozen until April 2028.

- The 45p ‘additional rate’ tax band threshold will reduce from £150,000 to £125,140 from 6 April 2023.

- The dividend allowance will reduce from £2,000 to £1,000 from April 2023 and then to £500 from April 2024.

- The capital gains tax allowance will reduce from £12,300 to £6,000 from April 2023 and then to £3,000 from April 2024.

- The stamp duty changes implemented as a result of the ‘mini-budget’ will now be temporary and will end in April 2025, at which point they will revert to their old limits.

- The VAT registration threshold will be frozen at £85,000 until March 2026.

- Research and development tax reliefs for small and medium sized enterprises (SME) will be reduced for spend after April 2023, but increased for businesses not qualifying for the SME scheme.

- The energy price guarantee will continue from April 2023 to April 2024, albeit with a higher typical bill limit of £3,000 per annum (up from £2,500). There will also be lump sum payments to those on certain benefits, pensioners and the disabled.

- There will be a treasury review to determine the support for energy bills to be offered to businesses from next April.

- Benefits, including the state pension, will increase by inflation (10.1%) from next April.

- The national living wage will increase from £9.50 to £10.42.

- In the accompanying documentation, company car and van benefit rates to April 2028 were also set.

- Electric cars will start to be subject to vehicle excise duty (road tax) from April 2025.

To expand on some of the changes in more detail:

Income tax and national insurance

The rates of income tax and national insurance remain unchanged from their current (ie post 5 November) levels, which are the same as they were in 2021-22.

The tax and national insurance thresholds, apart from the 45% tax threshold, will be frozen at current levels until April 2028.

The 45% tax threshold will reduce from £150,000 to £125,140.

There is a reason for the seemingly odd figure of £125,140: for income above £100,000, £1 of personal allowance is lost for every £2 of income, giving an effective tax rate for earned income between £100,000 and £125,140 of 60%, so the 45% threshold has been set at the top of this band.

Dividend tax

The rates of tax for dividends will remain at 8.75%/33.75%/39.35% (basic/higher/additional).

The dividend allowance will reduce from £2,000 to £1,000 from April 2023 and then to £500 from April 2024.

Capital gains tax

Capital gains tax remains at 10% (for gains falling into the basic rate band) and 20% (higher rate) (18%/28% for residential property gains).

The capital gains tax allowance will reduce from £12,300 to £6,000 from April 2023 and then to £3,000 from April 2024.

Research and development tax relief

There will be changes to research and development tax reliefs from April 2023.

For small and medium sized enterprises, the enhanced deduction will be reduced from 130% to 86% and the repayable credit cut from 14.5% to 10%.

For businesses not qualifying for the SME scheme, relief will increase from 13% to 20%.

The government will consult on the design of a single scheme for all businesses.

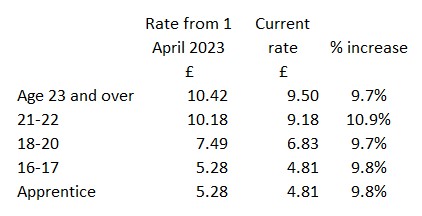

National Minimum/Living Wage

The new rates will be as follows:

Car and van benefit rates

The government is setting rates for Company Car Tax until April 2028. Rates will continue to incentivise the take up of electric vehicles.

The appropriate percentages for electric and ultra-low emission cars emitting less than 75g of CO2 per kilometre will increase by 1 percentage point in 2025-26; a further 1% in 2026-27 and a further 1% in 2027-28 up to a maximum appropriate percentage of 5% for electric cars and 21% for ultra-low emission cars.

Rates for all other vehicles bands will be increased by 1 percentage point for 2025-26 up to a maximum appropriate percentage of 37% and will then be fixed in 2026-27 and 2027-28.

Car and Van Fuel Benefit Charges and van benefit charge will increase in line with CPI from April 2023.

Vehicle Excise Duty (VED)

From April 2025, electric cars, vans and motorcycles will begin to pay VED in the same way as petrol and diesel vehicles:

- new zero emission cars registered on or after 1 April 2025 will be liable to pay the lowest first year rate of VED (which applies to vehicles with CO2 emissions 1 to 50g/km) currently £10 a year. From the second year of registration onwards, they will move to the standard rate, currently £165 a year

- zero emission cars first registered between 1 April 2017 and 31 March 2025 will also pay the standard rate

- the Expensive Car Supplement exemption for electric vehicles is due to end in 2025. New zero emission cars registered on or after 1 April 2025 will therefore be liable for the expensive car supplement. The Expensive Car Supplement currently applies to cars with a list price exceeding £40,000 for 5 years

- zero and low emission cars first registered between 1 March 2001 and 30 March 2017 currently in Band A will move to the Band B rate, currently £20 a year

- zero emission vans will move to the rate for petrol and diesel light goods vehicles, currently £290 a year for most vans

- zero emission motorcycles and tricycles will move to the rate for the smallest engine size, currently £22 a year

- rates for Alternative Fuel Vehicles and hybrids will also be equalised