The Chancellor, Jeremy Hunt, presented his Budget statement on 6 March 2024.

The main announcements relating to individuals and small businesses were:

- Personal tax and National insurance:

- Employee national insurance was reduced from 12% to 10% in the Autumn Statement, with effect from 6 January 2024. The Chancellor announced a further reduction to 8%, to take effect from 6 April 2025.

- Class 4 national insurance (paid by the self employed) will reduce from its current rate of 9% to 6% from 6 April 2024. (It was due to reduce to 8% from 6 April following the Autumn Statement).

- All main income tax and national insurance threshold remain unchanged from the current tax year.

- Child Benefit:

- The starting threshold for the High Income Child Benefit Charge will increase from £50,000 to £60,000. It will taper over income up to £80,000 (increased from £60,000), so the rate of withdrawal will be halved. These are the first increases in the thresholds since it was introduced in January 2013!

- The Government will consult on moving to a household based system from April 2026 (this is likely to be a challenge since there is no way of implementing this based on the current tax system).

- Landlords and property:

- The higher rate of capital gains tax for residential properties will reduce from 28% to 24% with effect from 6 April 2024. The lower rate remains at 18%.

- The Furnished Holiday Lets regime will be abolished from April 2025.

- SDLT multiple dwellings relief will be abolished from 1 June 2024 (these were rules that allowed less stamp duty to be paid if more than one property was bought at once – eg a block of flats).

- ‘Non-Doms’

- The current ‘Non-Doms’ tax system (which, in simple terms, deals with tax for individuals living in the UK who were not born here) will be abolished from April 2025. Non-Doms will start to pay the same tax as UK residents after 4 years of residency.

- Savings

- The government annoucned its intention to introduce a new UK ISA with its own allowance of £5,000 a year. They will consult on the details at a later date.

- VAT

- The VAT registration threshold will increase from £85,000 to £90,000 from 1 April 2024. The deregistration threshold will be £88,000.

- Other indirect taxes

- Fuel and alcohol duties will be frozen for another year

- A new vaping profucts duty will be increased from 1 October 2026, alongside a proportionate increase in tobacco duties.

Confirmation of the personal tax rates and allowances for 2023-24 can be found here: Annex A

Previous announcements taking effect/continuing from April 2024:

- Most income tax, national insurance and inheritance thresholds remain frozen until April 2028.

- The dividend allowance will reduce from £1,000 to £500 from April 2024

- The capital gains tax allowance will reduce from £6,000 to £3,000 from April 2024.

- Compulsory class 2 contributions will no longer be payable from 5 April 2024 – individuals will still be able to pay voluntary class 2 to maintain their national insurance record where their profits are below the small profits threshold.

- The Government will consult on the full abolishment of Class 2 national insurance later this year.

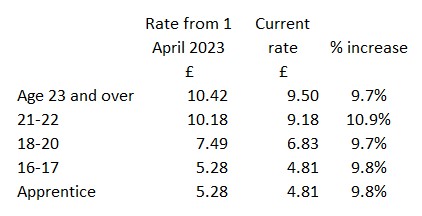

- The national living wage will increase from £10.42 to £11.44 from 1 April 2024, and those aged 21 and over will be entitled to the full rate (previously, those aged 21-22 could be paid a lower rate). Details of the rates by age/category can be found here

- Electric cars will start to be subject to vehicle excise duty (road tax) from April 2025.

To expand on some of the changes in more detail:

Income tax and national insurance

Apart from the reduction in the rates of employee and self employed national insurance, the rates of income tax and national insurance remain unchanged from their current levels.

The main tax and national insurance thresholds will be frozen at current levels until April 2028. (Some allowances, such as the blind person’s allowance, continue to be uprated in line with inflation).

Dividend tax

The rates of tax for dividends will remain at 8.75%/33.75%/39.35% (basic/higher/additional).

The dividend allowance will reduce from £1,000 to £500 from April 2024.

Capital gains tax

Capital gains tax for non-residential proprty gains remains at 10% (for gains falling into the basic rate band) and 20% (higher rate).

The rates for residentual property will be 18% and 24% (reduced from 28%).

The capital gains tax allowance will reduce from £6,000 to £3,000 from April 2024.

Furnished Holiday Lets (FHL)

The Furnished Holiday Lets regime will be abolished from April 2025.

The current benefits of FHLs are:

- Interest charges are deductible from profits at marginal rates of tax rather than being restricted to 20% as they are for residential property lettings

- You can claim Capital Gains Tax reliefs for traders (Business Asset Rollover Relief, Entrepreneurs’ Relief, relief for gifts of business assets and relief for loans to traders)

- You’re entitled to plant and machinery capital allowances for items such as furniture, equipment and fixtures

- The profits count as earnings for pension purposes

The abolishment will mean that furnished holiday lets will lose these benefits and be taxed in the same was as standard residential lets:

- Interest will not be deductible from profits, it will be subject to the same restriction to 20% as existing residential lets

- Capital gains tax will be at higher rates and will not benefit from trade reliefs

- Furnishings and fixtures will only be deductible as and when they are replaced

- Landlords relying on FHL income to provide relevant earnings for their pension contributions will no longer be able to do so.

Car and van benefit rates

In March 2023, the government set rates for Company Car Tax until April 2028. The rates continue to incentivise the take up of electric vehicles.

The appropriate percentages for electric and ultra-low emission cars emitting less than 75g of CO2 per kilometre will increase by 1 percentage point in 2025-26; a further 1% in 2026-27 and a further 1% in 2027-28 up to a maximum appropriate percentage of 5% for electric cars and 21% for ultra-low emission cars.

Rates for all other vehicles bands will be increased by 1 percentage point for 2025-26 up to a maximum appropriate percentage of 37% and will then be fixed in 2026-27 and 2027-28.

Car and Van Fuel Benefit Charges and van benefit charge will increase in line with CPI from April 2023.

Vehicle Excise Duty (VED)

From April 2025, electric cars, vans and motorcycles will begin to pay VED in the same way as petrol and diesel vehicles:

- new zero emission cars registered on or after 1 April 2025 will be liable to pay the lowest first year rate of VED (which applies to vehicles with CO2 emissions 1 to 50g/km) currently £10 a year. From the second year of registration onwards, they will move to the standard rate, currently £165 a year

- zero emission cars first registered between 1 April 2017 and 31 March 2025 will also pay the standard rate

- the Expensive Car Supplement exemption for electric vehicles is due to end in 2025. New zero emission cars registered on or after 1 April 2025 will therefore be liable for the expensive car supplement. The Expensive Car Supplement currently applies to cars with a list price exceeding £40,000 for 5 years

- zero and low emission cars first registered between 1 March 2001 and 30 March 2017 currently in Band A will move to the Band B rate, currently £20 a year

- zero emission vans will move to the rate for petrol and diesel light goods vehicles, currently £290 a year for most vans

- zero emission motorcycles and tricycles will move to the rate for the smallest engine size, currently £22 a year

- rates for Alternative Fuel Vehicles and hybrids will also be equalised